Ari Widodo

Introduction

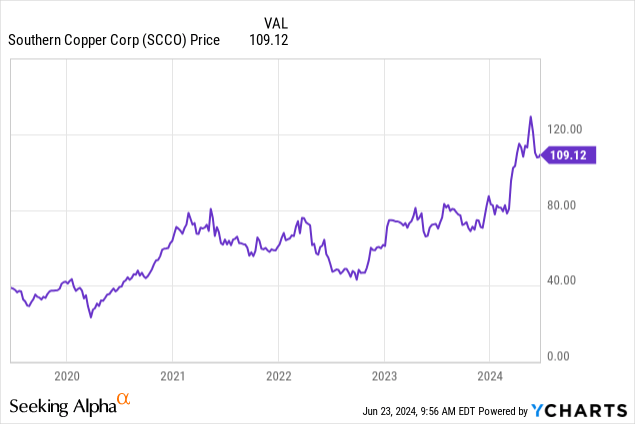

Southern Copper Corporation (NYSE:SCCO) is one of the world’s largest copper producers, with extensive mining operations in Peru and Mexico. With the ongoing push towards electrification, demand for copper is set to grow significantly, and combined with supply constraints, the price of copper looks set to increase. Now could be the perfect time to gain exposure to this crucial commodity. With some of the largest copper reserves and mine lives in the industry, combined with a focus on expanding production capacity, Southern Copper looks well placed for the future. Over the past 5 years, the shares have risen by 180%, reflecting strong performance. But the question remains: is Southern Copper stock a buy today?

Company Overview

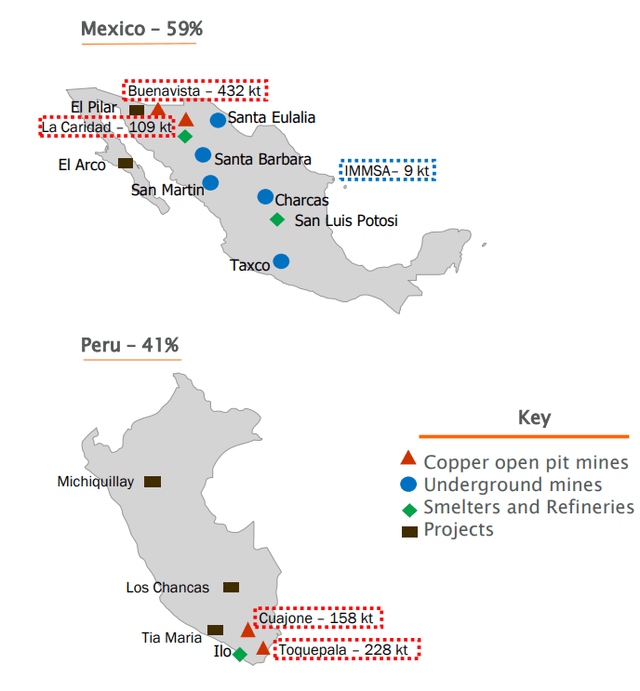

Southern Copper Corporation is one of the largest copper miners in the world. With roots tracing back to 1952, its modern form came into being with the acquisition of the Southern Peru Copper Corporation by the Mexican copper producer Minera México in 2005. Now majority owned by Grupo México, which holds an 88.9% ownership stake, Southern Copper operates mining assets in both Mexico and Peru.

SCCO Q1 2024 Presentation

Amongst its competitors, Southern Copper offers several advantages. Southern Copper’s extensive reserves at 44.8 million tonnes are amongst the highest in the industry, supporting the company’s long-term viability. These vast reserves, combined with long mine lifetimes, provide Southern Copper with a stable production outlook and operational stability.

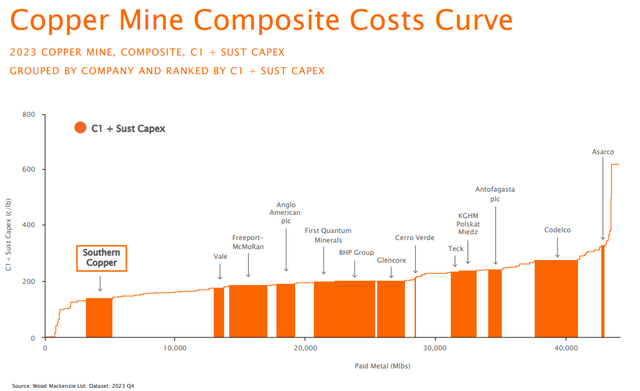

Another key advantage distinguishing Southern Copper from its competitors is its status as one of the lowest-cost producers in the industry. This provides a significant advantage, especially in commodity bear markets. This enables Southern Copper to remain profitable during periods of lower copper prices, unlike marginal producers.

SCCO Q1 2024 Presentation

As the producer of a globally traded commodity, Southern Copper is a price taker with no pricing power, making it heavily exposed to the price of copper. When copper prices rise, Southern Copper observes a greater percentage profitability increase due to operational gearing. The opposite is the case when copper prices decrease. However, when prices decline, the company’s earnings are less affected than those of higher-cost producers, due to its status of being one of the lowest-cost producers.

Surging Demand for Copper

Copper’s soaring demand, driven by electrification and growing renewable energy deployment significantly benefits Southern Copper Corporation. With its excellent electrical conduction properties, copper is the metal of choice for electrification. I covered this burgeoning demand in more detail in my previous article on the COPX ETF (COPX) where I explained how the energy transition is a major driver of demand for copper:

Electric vehicles are predicted to use 2-3 times as much copper as their traditional counterparts. In power generation, for solar seven times as much copper is needed to produce the same power as traditional power generation. For wind power that figure is seven times as much.”

With many governments implementing policies promoting renewable energy and phasing out combustion engine vehicles in favour of EVs, demand for copper is only set to grow. S&P Global is predicting demand for copper could double by 2035 as electrification efforts accelerate.

However, the supply side of copper is failing to keep up with this demand. Producers such as Southern Copper face challenges with growing supply significantly. Exploration budgets have fallen, environmental regulations have tightened, and opposition to new projects has grown. This has led to fewer new mines and longer timescales to bring a new mine online. This has led to miners favouring expansion of existing mines over new ones, with analysts estimating copper prices need to rise over 20% from recent highs to encourage greater investments in new mining ventures.

For Southern Copper, these dynamics create a favourable market environment. Booming demand combined with constrained supply, is likely to result in higher copper prices in the future, increasing Southern Copper’s revenue and profits. With Southern Copper’s vast reserves and expansion initiatives, combined with its position as one of the lowest-cost producers in the industry, Southern Copper should maximise gains from a higher copper price.

Boosting Production

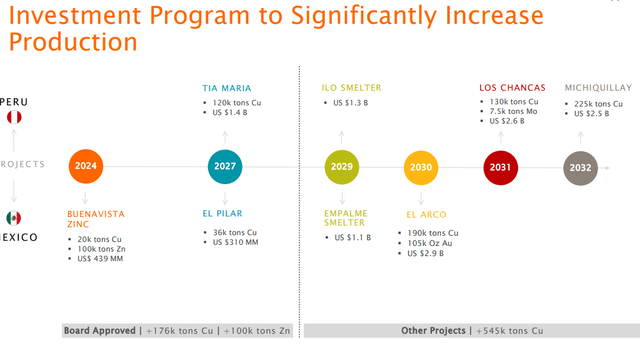

With the bullish outlook for copper prices, Southern Copper is well positioned to capitalise on this growth. Despite expanding and opening new mines becoming increasingly harder, Southern Copper has a clear pipeline of developments aimed at increasing its production capacity. Southern Copper forecasts its copper production increasing 78% over the next decade, from 911,000 metric tonnes in 2023 to 1,621,000 metric tonnes produced in 2032. This comes through both the expansion of existing mines and the opening of new mines. As a result of this growth in production, capital expenditure is set to rise over the coming years from an estimated $1.16 billion in 2024 to $2.67 billion a year in 2030.

SCCO Q1 2024 Presentation

This growth in production has not come without its challenges. The large Tia Maria project in Peru, which is set to produce 120,000 metric tonnes of copper annually, has long-faced problems. The mine has faced major protests and opposition over the mine’s environmental impact from local communities. After protests in 2019, the Peruvian government suspended the construction licence for 120 days. Now, after almost a decade of delays, the project is finally set to start construction in early 2025.

Other expansion projects have focused on current mine expansion, such as the Buenavista mine, which attracts much less opposition. With the copper price looking like it will rise in the future, opposition to new mines will hopefully decrease as both the state and local regions around the mines benefit from higher royalties.

With demand for copper set to soar and supply set to grow slower, higher copper prices look inevitable. With Southern Copper’s expansion initiatives, they should be able to take advantage of the higher prices, helping boost revenue and profits into the future. Despite challenges faced in expanding production, Southern Copper looks set to play a key role in meeting growing global demand for copper.

Q1 Results

Southern Copper released its results for Q1 at the end of April. Let’s first look at the production numbers reported.

SCCO Q1 2024 SEC filing

Overall copper production in the first quarter increased 7.6% year-on-year. This was largely due to a 22.2% increase in production at the Toquepala mine from higher ore grades and recoveries. Other mines also saw smaller increases with production up around 13% at both the Cuajone and La Caridad mines. This offset the 3% fall at the large Buenavista mine which faced drops in ore grades.

Other metals also saw increased production, with Zinc production up by 74.9%. This is attributed to the production start-up at the Buenavista zinc concentrator, which produced 9,695 tonnes during the quarter. Overall copper represented 78.6% of sales by value in the quarter, followed by Molybdenum at 10.5%, with the rest made up of Zinc, Silver, and other byproducts.

In the first quarter of Q1 Southern Copper achieved net sales of $2.6 billion, down 6.9% on the year. This translated into net income of $736 million, down 9.5% from the $813 million reported the previous year. Operating expenses fell $30 million year-on-year driven by lower cost of sales. This led to earnings per share coming in at $0.94 beating expectations by $0.19.

SCCO Q1 2024 SEC filing

Although volumes of metals sold were up in the quarter, revenue fell due to lower metal prices compared to a year earlier, with the average copper prices being down 5.4% on the year. Although copper prices recently surged and reached new highs, most of these gains occurred at the tail end of Q1 and during Q2. As such the benefit from these higher copper prices won’t be included until second quarter results.

In the first quarter, Southern Copper invested $213.8 million in capital expenditure to help maintain and grow production.

Overall, the results presented a mixed picture. While production volumes and cost control were strong, revenue was impacted by a lower metal price. These results reinforce the company’s dependence on the metal price. With the copper price having risen since, the second quarter should show improved results.

Q2 Outlook

Southern Copper is set to report its results for Q2 2024 at the end of July. Current expectations are for revenue of $2.75 billion, a rise of just over 19% compared to the same quarter in the previous year. Earnings per share is set to come in at around $0.99, an increase of 42%. This comes on the back of the record high in the copper price seen during the quarter, leading to a higher realized sale price for Southern Copper’s products.

Valuation

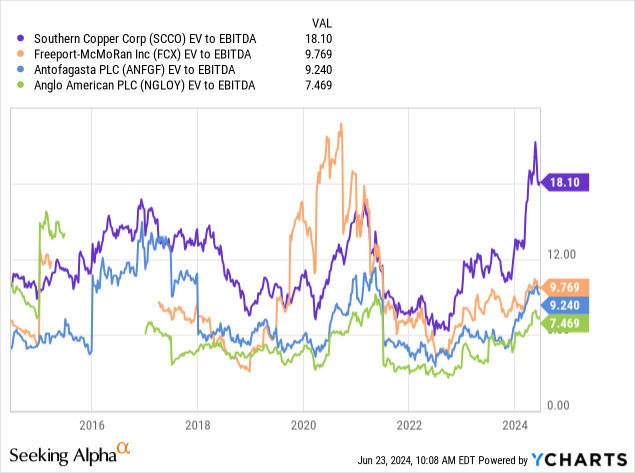

Placing a valuation on a copper miner is hard given the earnings dependence on the price of copper. As such I believe the fairest way to value the company is in comparison to other large copper miners such as Freeport-McMoRan (FCX), Anglo American (OTCQX:NGLOY), and Antofagasta (OTC:ANFGF). Given the large difference in cash and debt levels, a direct comparison of earnings multiples will not suffice, and I instead use an enterprise value to EBITDA multiple.

When compared to its peers, we see that Southern Copper trades at a significant premium with an EV/EBITDA multiple of 18.1 with all peers having a multiple under 10. Additionally, this multiple is the highest in the past 10 years and well above the company’s average multiple.

While a premium may be justified due to Southern Copper’s status as a low-cost producer with substantial reserves, it raises questions about the stock’s upside potential. Although I am bullish on the copper price in the long term and believe Southern Copper has a bright future ahead, the valuation is too high for me to consider an investment presently. As such I assign a “Hold” rating to the shares.

Risks

When considering an investment in Southern Copper, there are two main risks, I believe it is important to consider: copper price volatility and geopolitical uncertainty.

Firstly, copper price volatility. Southern Copper’s financials are deeply dependent on the price of copper, its primary source of revenue. As such, changes in the price of copper will deeply impact the revenue and profits of the company. Although I am bullish on the copper price in the long term and copper achieving a recent high in the copper price, global economic factors and industrial demand can drive prices in the short term. For instance, recent falls from the record high can be partly attributed to stockpiling and a manufacturing slowdown in China. While the long-term outlook for copper prices remains positive from electrification initiatives, short-term factors could cause reductions in the copper price, impacting Southern Copper’s earnings.

Secondly, geopolitical factors. Copper mining is subject to various geopolitical and regulatory risks, from having to meet ever increasing environmental standards, risks of higher royalties, and other regulations increasing costs. In some cases, this has led to mine closures, such as that of First Quantum Minerals (OTCPK:FQVLF) mine in Panama. Although Southern Copper primarily operates in Peru and Mexico, fairly well-respected mining jurisdictions, this remains a challenge as governments change. Recently, the Mexican government proposed the banning of new open pit mines, which coincides with the increasing difficulty of obtaining new mining permits. Geopolitical risks are part and parcel of the mining industry and something investors should monitor.

Conclusion

Southern Copper Corporation looks set for a bright future. It is one of the best copper miners out there, with vast reserves and plans in place to support future production growth. Combined with the positive outlook for the copper price as the metal of electrification, Southern Copper’s earnings should benefit. However, at the current share price, the company’s valuation appears elevated. As such, I assign the shares a “Hold” rating. I will continue to monitor the company’s performance and will consider an investment if the valuation becomes more attractive.

")

{kind=link}